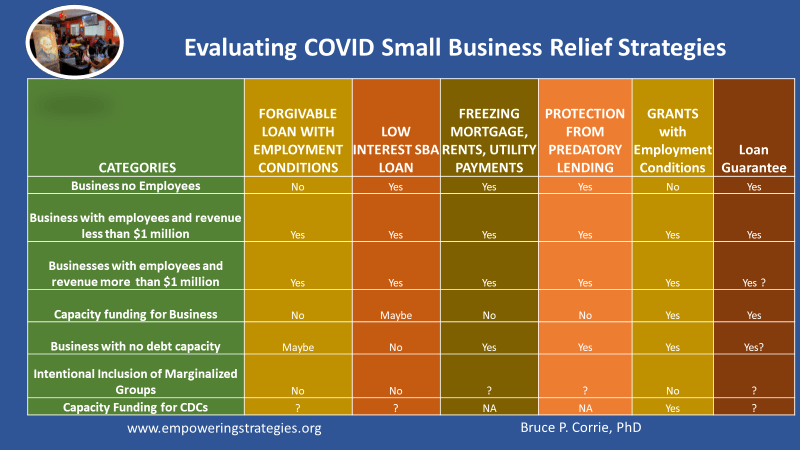

A number of relief strategies are being proposed or implemented by governments to help businesses during the COVID-19 virus crisis. So how can we assess the effectiveness of these strategies on small businesses? This article suggests a simple scorecard to assess the breadth and depth of these strategies illustrated in the graphic above.

There is a wide range of businesses from independent contractors and consultants to large businesses. So we have to explore the possible impact on each of these business types to ensure that the economic relief serves the purpose it was intended. The categories identified are: small businesses with no employees (which includes consultants and other independent contractors as well as the Mom and Pop stores in the neighborhood), small businesses with revenue less than a million dollars with employees, small businesses with revenue greater than a million dollars and with employees.

The scorecard also includes four other elements important for the survival of small businesses during this crisis.

First, the business must have the capacity to take on debt. Many businesses are struggling to repay their current loans and cannot afford to take on a new loan even with a low interest rate.

Second, in order for these economic relief strategies to work the business should also have the capacity to turn around their business model to cater to customers during the downtime in order to bring in some revenue. For example a restaurant that changes its model to “take-out” or “delivery” would need to have a website, partnership with delivery services and capacity to receive orders and fulfill them at a different scale than serving a small room with 50 customers at a time.

Third, minority and other disadvantaged businesses already face a number of barriers as they access programs and resources. Will this new program address those barriers and provide access to these programs?

Fourth, the program should include capacity building for business supporting organizations working with small and minority businesses to access and use these resources.

Let’s evaluate some of the popular programs proposed and adopted by a wide range of governments. “Yes” or “No” in the table indicates if it will or will not work for that business or category.

Forgivable Loans

The forgivable loan program offers a zero or low interest loan forgivable partially or fully if the employer retains employees during the crisis.

In evaluating this program with the scorecard one can see it leaves out some of the most vulnerable businesses that have no employees. They do not include capacity development funding and do not indicate an intentional focus on inclusion of minority and disadvantaged businesses. Some address the latter through partnership with community development organizations which serve minority and other disadvantaged businesses. This type of loan might be accessible to a business without any debt capacity because of its forgivable component.

SBA Disaster Loans

These loans carry a long term and very low interest rates (3.75 percent) and is open to any business. However it will not work for a business over its debt capacity, nor does it include resources to build capacity of businesses, or an intentional effort at inclusion.

Freezing Foreclosures, Property taxes, Mortgage payments, Rents, Utility payments

These policies will serve a wide range of businesses especially the most vulnerable as it helps stop the bleeding by freezing some fixed costs. Many businesses are on the verge of bankruptcy and may have only a month’s cushion before they collapse. These programs need to be combined with forgivable and SBA disaster loans to be effective and integrate a strategy of intentional inclusion. While these kinds of programs have been adopted for homeowners and renters they have not explicitly included small business owners.

Predatory Lending

Many businesses will be vulnerable to predatory lenders and currently there is little protection for business owners caught up in these types of loans. Many of these loans prevent the business owner from seeking protection for their assets. Minority and other disadvantaged businesses are especially vulnerable as they do not have good access to capital. The Responsible Business Lending Coalition offers a Small Business’ Borrower Bill of Rights as a first step in protection from predatory lenders. Consumers have more protection against predatory lending than small business owners.

Grants

Grants are offered to small businesses without many restrictions to allow the businesses resources to pay for a wide range of costs such as mortgage payments, utilities etc. They might have an employment condition in some forms.

Loan Guarantees

To share loan risk during this crisis, governments offer loan guarantees for small business loans. These loans can be for a wide range of uses and for businesses with or without employees.

The above scorecard can help evaluate various types of economic relief programs aimed at small businesses during the COVID crisis and suggests a comprehensive framework to include all these elements in an effective strategy aimed at business relief, protection and development.

The author is an economist and served as the director of Planning and Economic Development for the City of Saint Paul, Minnesota. He has extensive experience working with minority and immigrant owned businesses.

Tags: #covid #covid-19 #forgivable #loans #small #business #minority #predatory #lending #SBA #disaster #foreclosure #mortgage #rent #low-income #economic #development #scorecard