The board of the Union Park District Council adopted the Small Business Borrowers’ Bill of Rights as a first step against the increasing presence of predatory lending in Saint Paul. Recently three community lenders, MEDA, AEDS and CRF together with the City of Saint Paul and Vision Bank, helped rescue a female African immigrant small business owner from the snares of a predatory lender who charged her over 200 percent in interest and fees. The process took six grueling months as the lenders and the business owner tried to finance a rescue loan package. The most ironic moment was in the heart of the COVID-19 crisis when the loan was to be closed the predatory lender increased, rather than decreased the loan amount.

The resolution adopted by the board of the Union Park District Council affirmed a Borrowers Bill of Rights (see summary below) and called on both the City of Saint Paul and the State of Minnesota to adopt a similar resolution as the first step against predatory lending. Board members expressed concern that in during the COVID-19 crisis when many small businesses are in financial crisis, they run the risk of being ensnared by predatory lenders. The resolution was developed in partnership with the national Small Business Lending Coalition.

A number of local lenders have adopted the Small Business Borrowers’ Bill of Rights and include, MEDA, AEDS, Hmong American Partnership (HAP), Metropolitan Consortium for Community Development (MCCD), Neighborhood Development Center (NDC), African Development Center (ADC) and Hmong American Partnership (HAP). Congressman Dean Phillips (D-MN-03) introduced a federal resolution in support of the Rights in 2019, along with Congressman William Timmons (R-SC-04) and House Small Business Committee Chairwoman Nydia Velazquez (D-NY-07).

Small Business Borrower Bill of Rights (http://www.borrowersbillofrights.org/)

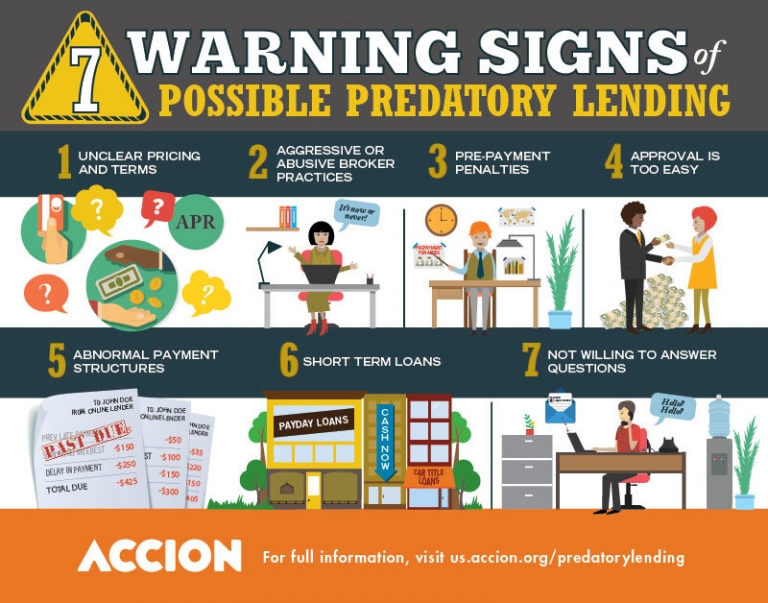

1. The Right to Transparent Pricing and Terms: A borrower has the right to have the cost and terms of any financing being offered presented to them in writing and in a form that is clear, complete, and easy to compare with other financing options, so they can make the best decision for their business.

2. The Right to Non-Abusive Products: A borrower has the right to expect that the financing products offered by a lender will not trap his/her business in an expensive cycle of re-borrowing.

3. The Right to Responsible Underwriting: A borrower has the right to expect a lender is offering financing based on underwriting practices that assess the ability of the borrower’s business to succeed and repay.

4. The Right to Fair Treatment from Brokers: A borrower has the right to honest, transparent, and impartial communications with a broker regarding loan options, conflicts of interest, fees, and the financing options available.

5. The Right to Inclusive Credit Access: A borrower has the right to fair and equal treatment when seeking a loan including protections guaranteed under the Equal Credit Opportunity Act.

6. The Right to Fair Collections Practices: A borrower has the right to be treated fairly and respectfully throughout a collections process and the right to protections like those guaranteed under the Fair Debt Collection Practices Act.

#Predatory #lending #BillofRights #MinorityBusiness #Transparent #Pricing #COVID19